November 2024 - All about US politics

The US elections and Trump’s clean sweep was the main focus over the past month. Further rate cutting by both the Fed and SA’s MPC resulted in another 25bps decrease in interest rates.

Introduction

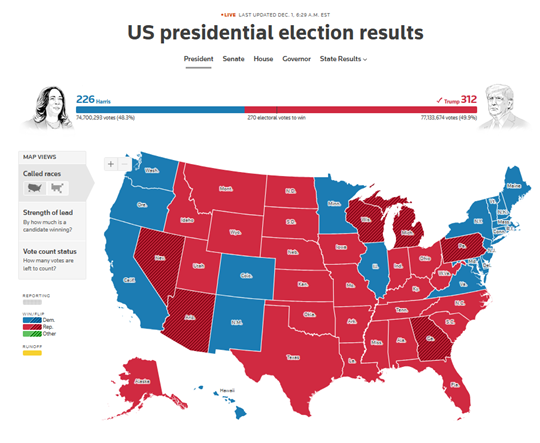

November was mainly about the US election and the clean sweep achieved by Trump and the Republicans. Trump has moved quickly in appointing members of his administration. The Treasury Secretary was the position that garnered the most attention with a number of names grabbing the spotlight. Following much speculation the market appeared happy with the choice of Scott Bessent for the role as he is seen as one of Wall Street and so may tone back some of Trump’s more extreme policies.

Outside of US politics there was a positive move in the Middle East with a 60 day ceasefire being agreed between Israel and Hezbollah which has provided some hope that there could be a move to a peaceful resolution in the region. On the other hand the Russia Ukraine war escalated with Russia making use of North Korean troops and Ukraine obtaining permission to use US long range missiles to hit targets within Russia. Trump has frequently mentioned that he will end the war although how that is meant to take place remains an unknown.

The general macroenvironment saw a continued rate cutting cycle with both the Fed and the South African MPC easing by 25bps. The big question is now whether the Fed cuts again in December or holds. There are some concerns that certain aspects of the economy are showing some inflationary signs and this coupled with Trump’s proposed policies could give room for the Fed to hold. This is despite many Fed speakers making it clear that they will not try and guess Trump’s policies and so they remain data dependent.

As the end of year approaches, strategists are starting to set price targets for the S&P500 for the end of 2025. Most strategists getting 2024 targets horribly wrong and needed several amendments during the year so we suggest that these targets are taken with a pinch of salt. However, in general the outlook is for a 10% return in 2025 which, off an already high base, would be a good achievement. The main driver is earnings and a continued soft landing macro environment. There is no doubt with Trump taking over the presidency and heightened geopolitical tensions we can expect and increase in volatility.

As we close out 2024 we have been pleased with portfolio performance on a risk adjusted basis. We are expecting 2025 to be a challenging year for markets with lots of moving parts but as always this will also present opportunities. The team is working hard to ensure portfolios are positioned appropriately and manage both the risk and the potential reward.

Macro Environment

The inflationary readings coming out the US have raised questions on the path of inflation and whether the last part may take longer to bring down to target. October Core PCE was in line with consensus rising 0.3% month on month and on an annualised basis was 2.8%. Headline was slightly lower at 0.2% month on month and 2.3% annualised. Interestingly on a monthly basis CPI was the same for core and headline whereas annualised core came in at 3.3%. Shelter continues to provide upward pressure on CPI, rising 0.4% and this is being watched closely by the market especially as housing market remains tight. The disinflationary trend remains in tact although some aspects are proving a bit sticky and so it may take a bit longer to reach the Fed target.

After the lead up to the election appearing tightly contested the result was anything but, with Trump and the Republicans taking a clean sweep of the Presidency, the House and the Senate. All of the swing states were lost by the Democrats and Trump even managed to win the popular vote unlike in 2016. Trump has hit the ground running although not officially in office yet he appears to be using aggressive tariffs as the first move in opening negotiations starting off by hitting Mexico and Canada with a blanket 25%. He also threatened the BRICS countries with a 100% tariff should they look to establish their own currency. There is no doubt his presidency is going to be filled with lots of noise that will impact markets.

Asset Allocation

Our local asset allocation remains unchanged as the local market looks for further momentum. Our offshore asset allocation has seen a down weighting to equity following the rally post the election. This has been centered around realizing some of the gains achieved from the performance this year. We have maintained bond allocation despite the recent volatility. In addition we have been adding to our Structured Notes position as an effective way to maintain equity exposure while providing some hedged protection with the US market looking a little stretched.

Market Performance

November was a very strong month for markets following the results of the election. During the month of November, the S&P 500 ended up 5.73%. The MSCI World index was up 4.76% for the month and the JSE saw a negative return of 1.02%. As per chart below the YTD performance of the JSE is up 9.91% (in ZAR), while the S&P500 is up 26.47% and the World index is up 21.76% (in USD), respectively.

Bonds

Bonds have seen an increase in volatility as the yield curve has been repositioning based on inflation expectations and in turn the Fed’s path. The outlook for a December cut has shifted significantly as the market moved from a 70% expectation of a cut to a 50% chance. Recent inflation readings have shown a slight uptick and while the economy remains strong the Fed will maintain their data dependent approach and various speakers have emphasised they do not feel a rush to cut. As outlined by the chart below the cutting cycle remains but the timing of cuts is a little more uncertain.

Equities

The third quarter earnings season is largely at a close and 75% of the S&P500 companies have reported a positive earnings surprise and 61% showed a positive revenue surprise. The blended earnings growth rate sits at 5.8%. For the fourth quarter there has been limited guidance although the guidance has been slightly more negative than positive. The forward PE of the S&P500 sits at 22x which is above the 5 year average (19.6) and the 10 year average (18.1). Generally companies saw a slight contraction in margins from a year ago although this was largely immaterial.

Going into Q4 the earnings outlook is very positive with a current expectation of 12% growth which would be more than double what was achieved in Q3. This positive momentum for earnings is also expected going into 2025 with the current expectations for all four quarters as follows 12.7%, 12.1%, 15.3% and 17.0%. S&P500 earnings growth from Q1 2022 through to Q4 2024 is reflected below.

This strong earnings growth outlook helps validate the high multiple that the S&P500 is currently demanding and is the main driver for the strong index forecasts that are currently being pushed out by the various Investment Banks.

Conclusion

As we look back on 2024 it has been a year driven by macro factors, politics, technology and geopolitical tensions. Regional and asset allocation has been critical with the US far out performing the likes of Europe and the UK. Bonds have seen a lot of volatility and equities have surpassed most experts forecasts. At DI we have been pleased with our positioning throughout the year and will be happy with a stable month in December to close out the year. We wish our clients a good Festive Break as we anticipate a busy year in 2025. Although the office will be closing on 20th of December and reopening on 6th January all portfolio managers will be available should clients need anything over the festive season.