A tough month in March 2025 fuelled by a steep sell-off and US trade policies

Market sentiment shifted dramatically due to the US falling out of favour with a number of investors, US stock driving sell-offs, and complex local budget processes.

Introduction

Markets saw a tough month in March with a steep sell off in US stocks being the main driver. The S&P 500 experienced its worst decline since December 2022. Growth and momentum stocks fell sharply, with major tech names like Meta (-13.7%), Nvidia (-13.2%), and Tesla (-11.5%) dragging down the market. Uncertainty around Trump's trade policies, including potential tariffs, dampened investor sentiment, while concerns over stagflation grew after the Fed revised its 2025 growth and inflation forecasts. Corporate earnings guidance also reflected cautious consumer and business sentiment. Despite the downturn, there were some positive signs, including strong consumer spending, resilient labor market data, and a weaker dollar, which eased earnings concerns. In Washington, a government shutdown was avoided.

In Europe, Germany announced a major infrastructure spending plan which helped boost the Euro market as sentiment turned positive. The main focus is on Defence as there is a clear need for Europe to have less reliance on the US. This spending has been well received by markets and is a fairly drastic shift away from Germany’s traditional fiscal constraint. Generally the European Union is seeing stronger unity as their relationship with the US faces strain.

Locally the SA Budget process for 2025 has been very complex with the initial budget presentation cancelled in February only for the Budget to be presented on 12 March following significant negotiations within the GNU. The main highlight from the speech was the announcement of the VAT rate increasing by 0.5% this year and a further increase of 0.5% the following year. This was seen as a compromise from the initial 2% proposed in the February budget version. The Treasury has forecast public debt peaking at 76.2% in the upcoming year and we would want to see this managed down from here. Currently the budget negotiations are still ongoing as the ANC and DA battle for ‘wins’. Over the weekend there was talk of the GNU collapsing around these negotiations as neither side were prepared to compromise. As of yesterday (Monday) a deal appeared imminent but is yet to be announced. For SA as a whole we need the Budget to be finalized in order to move forward as the uncertainty is not helpful.

Overall, market sentiment has shifted dramatically in March with the US falling out of favour with a number of investors and the uncertainty around trade policy and geopolitics creating a difficult investment landscape. We realise this is not an easy environment however, we believe we took actions on portfolios at the end of last year and must remain patient for opportunities to present themselves.

Macro Environment

As we face a shift back to a very uncertain macro environment we need to navigate these conditions focusing on the long term and not get caught up in the noise of short term news headlines. On the face of it a tariff war is not good for global markets as there is a strong positive correlation between global growth and global trade. Should the trade wars continue we should expect a slow down in global growth which won’t be good for risk assets. It is estimated that the tariff actions currently in effect by Trump could lower US GDP by up to 0.65%. As outlined by the Statista chart on the next page this is impacted by various elements but emphasizes the negative impact on growth.

Another element to keep watching is inflation and the labour market. There is a view that inflation could reverse course and start rising again. This coupled with a slow down in the labour market would not be positive and some commentators are warning of a stagflationary environment which would present a significant challenge for markets going forward. Goldman Sachs has increased their probability of a recession in the US to 35% as the administrations policies are having a negative overall impact.

To counter this US retail sales rose 0.2% in Feb which is a positive as almost 70% of GDP is driven by consumer spending and retail sales is a large chunk of this. Should consumers continue to spend then we would argue that a recession is unlikely. As outlined by the Statista chart below and on the right the consumer story will remain central to GDP and linked to this will also be their confidence. We continue to watch the macro data points unfold and are positioning portfolios accordingly.

Asset Allocation

Our local asset allocation remains unchanged. However, following a review the equity allocation is undergoing a shift to remain with a Rand hedge bias although and increase in diversification in the direct local exposure. Our offshore asset allocation also remains unchanged as we took action last year for the increased volatility. We have maintained the existing bond allocation. In addition, we have been adding to our Structured Notes position as an effective way to maintain equity exposure while providing some hedged protection.

Market Performance

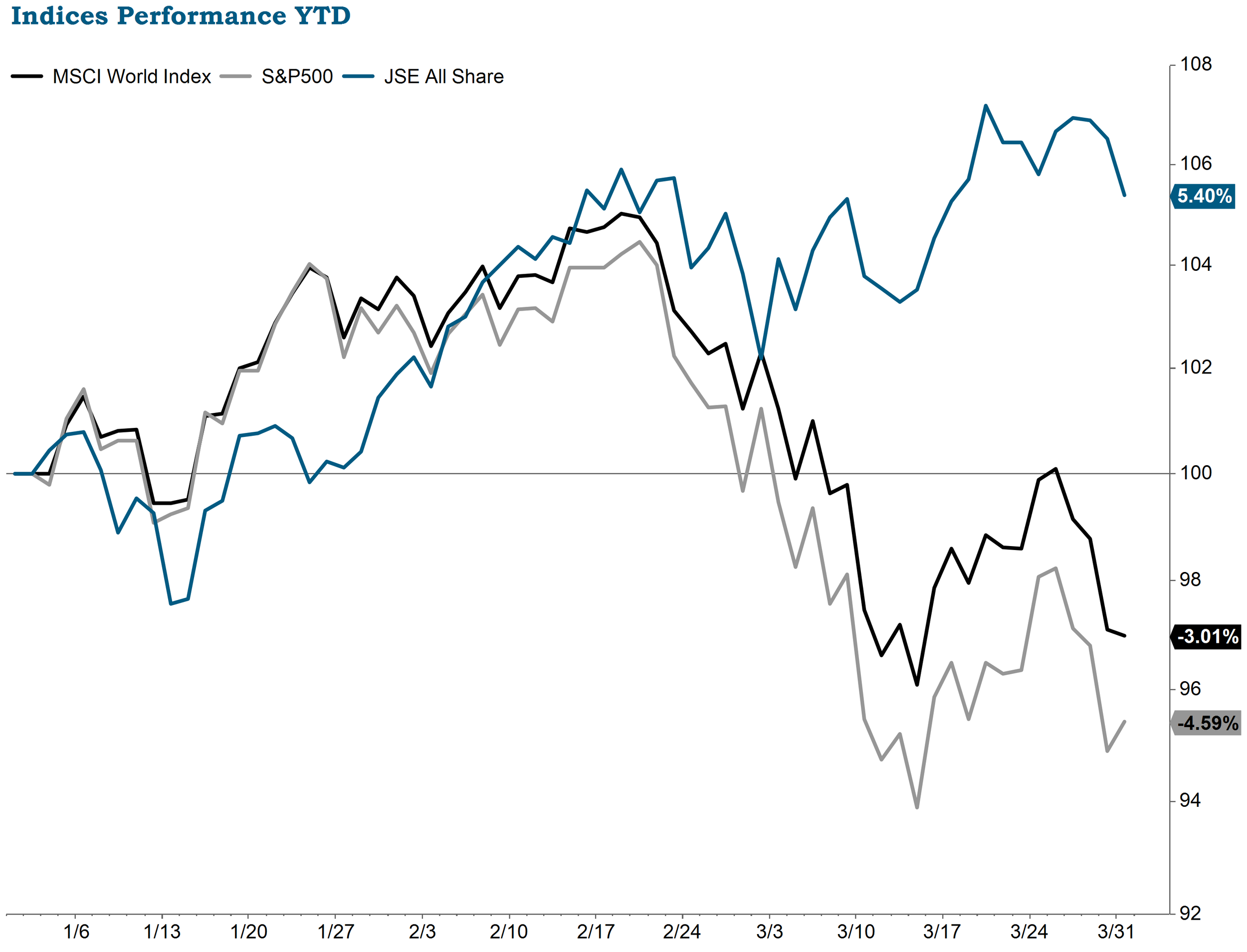

Generally, markets saw a negative month in March with the US being the main driver of the change in sentiment. The S&P500 was down 5.75% for the month, while the MSCI World was down 5.21%. The JSE was an outlier producing a positive 3.14% for March. As per the below chart the YTD performance for the S&P500 is down 4.59% (in USD) and the MSCI World is down 3.01% (in USD). Locally the JSE currently has a YTD performance of 5.40% (in ZAR).

Bonds saw some divergence in March with the US seeing a tightening of yields as there is an element of safe haven in Treasuries meanwhile the European Bond market saw rising yields as the significant stimulus announced by Germany will result in an increase in borrowing. As outlined by the chart below there was a steep rise in yields with some recovery towards month end. Locally the SA bond market saw a slight increase in the 10 year yield while the MPC kept the Repo rate at 7.5% largely in line with expectations.

Equities

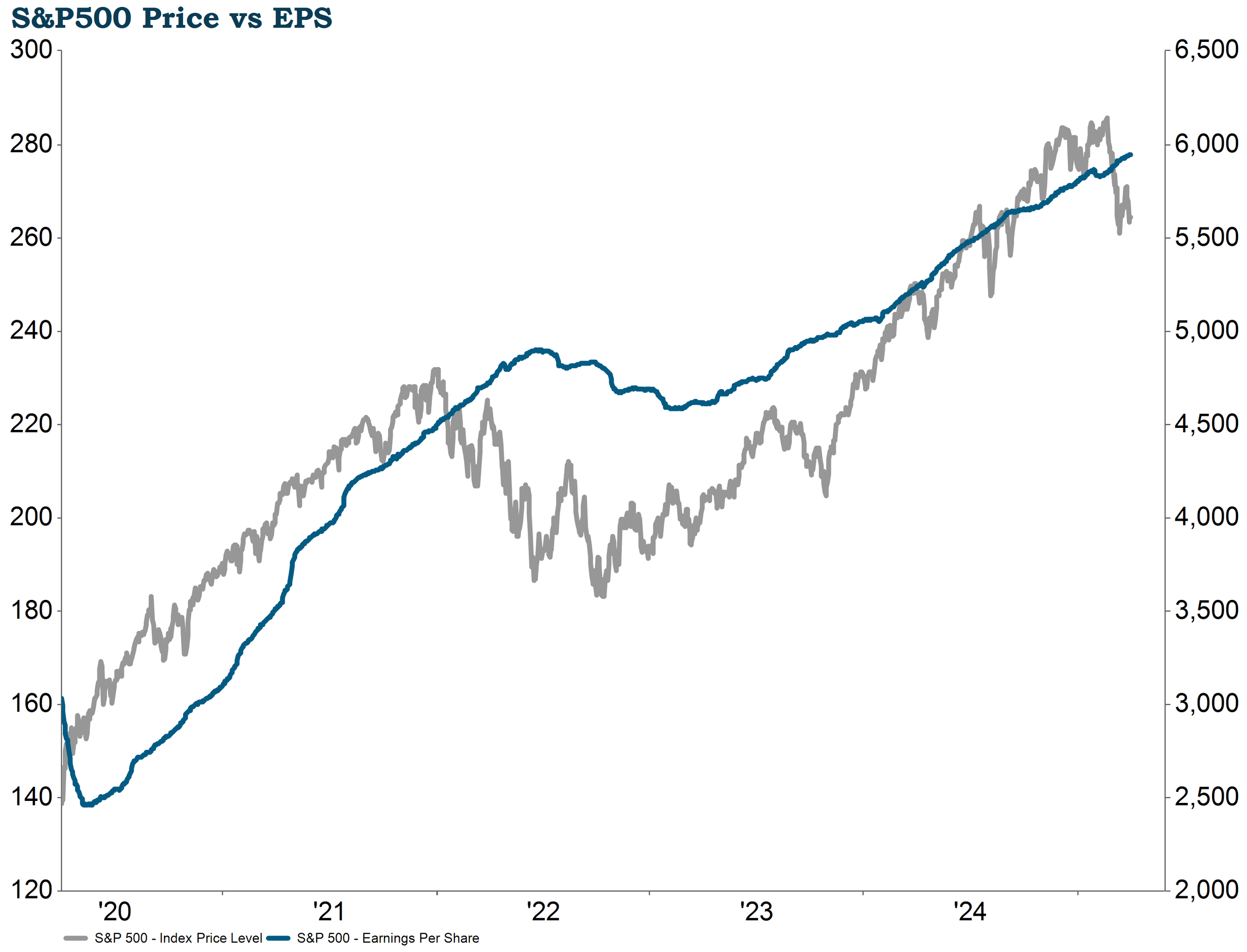

The sell off in US equities has largely been driven by the uncertainty in markets as the macro environment is changing daily. The tech sector has been the hardest hit as that is where valuations were the most stretched. However, this sell off could present an opportunity as outlined by the chart below there is a clear disconnect between the earnings trajectory and current price momentum. This emphasizes the importance of the coming earnings season where we will get insights into what companies are seeing on the ground. We have emphasized for a while now that equity valuations can only be supported by strong earnings so should this remain the case the current sell off is an opportunity however, a downgrade in earnings outlook will put further pressure on equity markets. A number of global strategists have downgraded their forecasts for the S&P500 for 2025 based on the current outlook. We were proactive at the end of 2024 and are now waiting to see what the next earnings cycle may provide before taking any action on portfolios.

Conclusion

We are back in an uncertain environment which naturally means increased volatility. We don’t expect this to change in the short term and hence it is important that we manage portfolios through the noise. We took action last year to protect portfolios and are now assessing where opportunities may present themselves by looking at longer term themes as opposed to the daily market moves. We understand that volatility is unsettling for our clients so please feel free to reach out to the team to discuss portfolio positioning and our views for the coming quarter.

Download Investment Environment Article (PDF, 601KB)